Rethinking Competitive Advantage in the Age of AI

Why software is becoming less of the moat, and why distribution and trust matter more than ever.

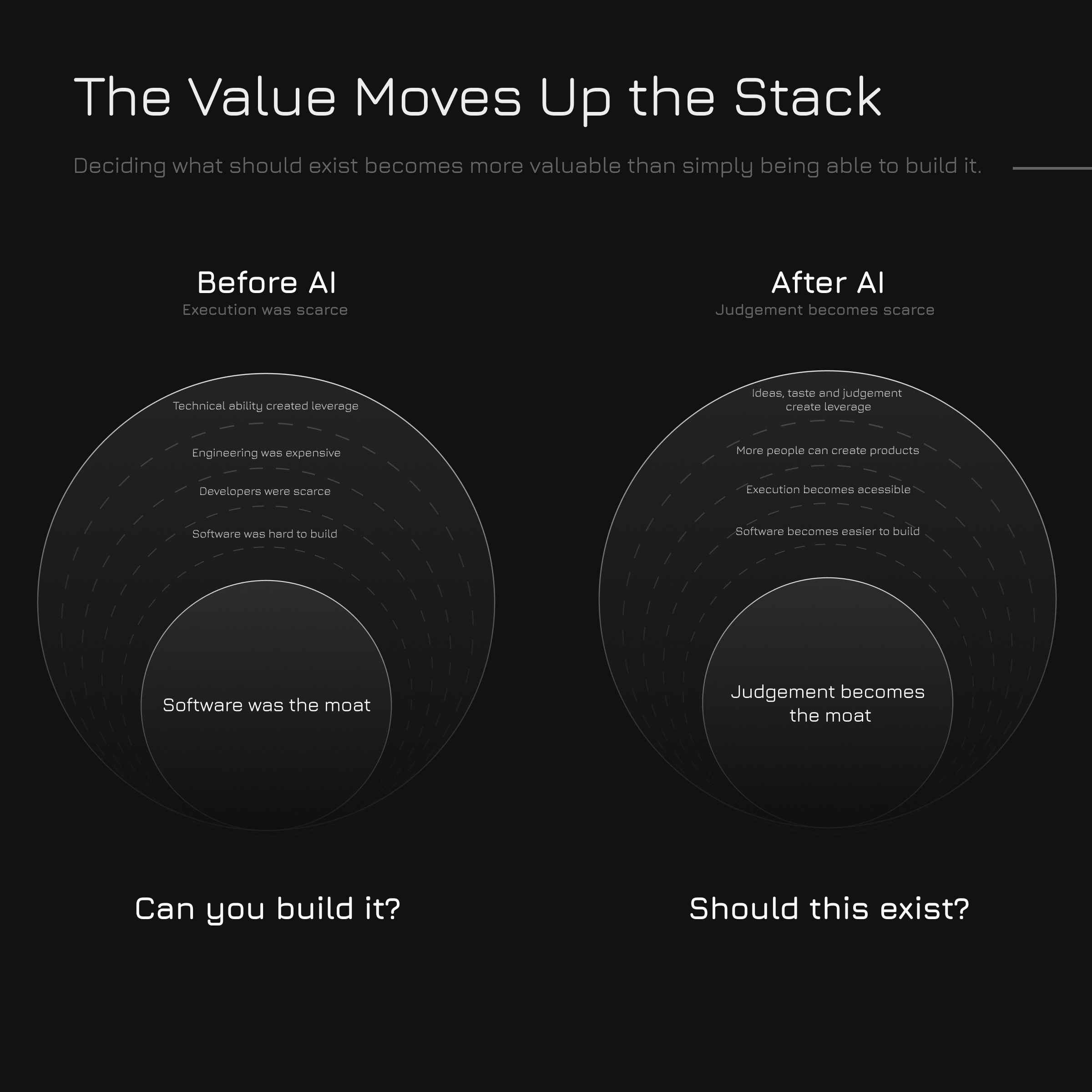

The Value Moves Up the Stack

As we were planning the investment thesis for Peers Capital, our recently launched syndicate, one of the assumptions we spent a lot of time thinking about is that, in an AI world, the value captured by software itself approaches zero.

That sounds more dramatic than I actually mean it. It’s not that I think software disappears. Quite the opposite. Software becomes even more important. What changes is where the value sits. For most of the last two decades, software itself was the moat because building it was hard.

Developers were scarce, engineering teams were expensive, and execution was often the biggest constraint to turning an idea into a company. If you had a good idea and the technical ability to build it, you had a meaningful advantage because very few people could actually execute on it.

AI has started to change that equation. Software isn’t just something developers build anymore. It’s becoming accessible to a much broader group of people who wouldn’t have considered themselves technical even a few years ago. Tools like Lovable and Claude are making it easier for people without a tech background to build products, and the pace of improvement has been striking. If you look at what these tools could do a year and a half ago compared to today, the progress is pretty remarkable. It’s still somewhat limited today, but the trajectory is clear.

GitHub’s research on Copilot found developers completed coding tasks around 56% faster with AI assistance, but the exact number isn’t really the point. The direction is. If you stretch that progress out over the next two to three years, it’s not unreasonable to think that technology becomes fully democratized, where anyone with a good idea can build a product. Building software is becoming dramatically easier, which means execution becomes less scarce. Assuming that’s true, I think something much bigger starts happening.

Historically, a disproportionate amount of value sat with the developer because execution was difficult. As that constraint weakens, the value shifts towards the product manager, or more broadly, towards the people shaping taste and direction rather than the people executing them.

Even technical decisions, such as what is better to build or how to implement something, can now be cross-validated with AI tools, which further reduces the advantage of pure execution. What cannot be outsourced in the same way is taste, and that is where differentiation increasingly lies. As a result, I think teams will become smaller and more focused on understanding communities and culture rather than purely understanding technology, because deciding what should exist becomes more valuable than simply being able to build it.

So if software itself is no longer the moat, it naturally raises another question: what is?

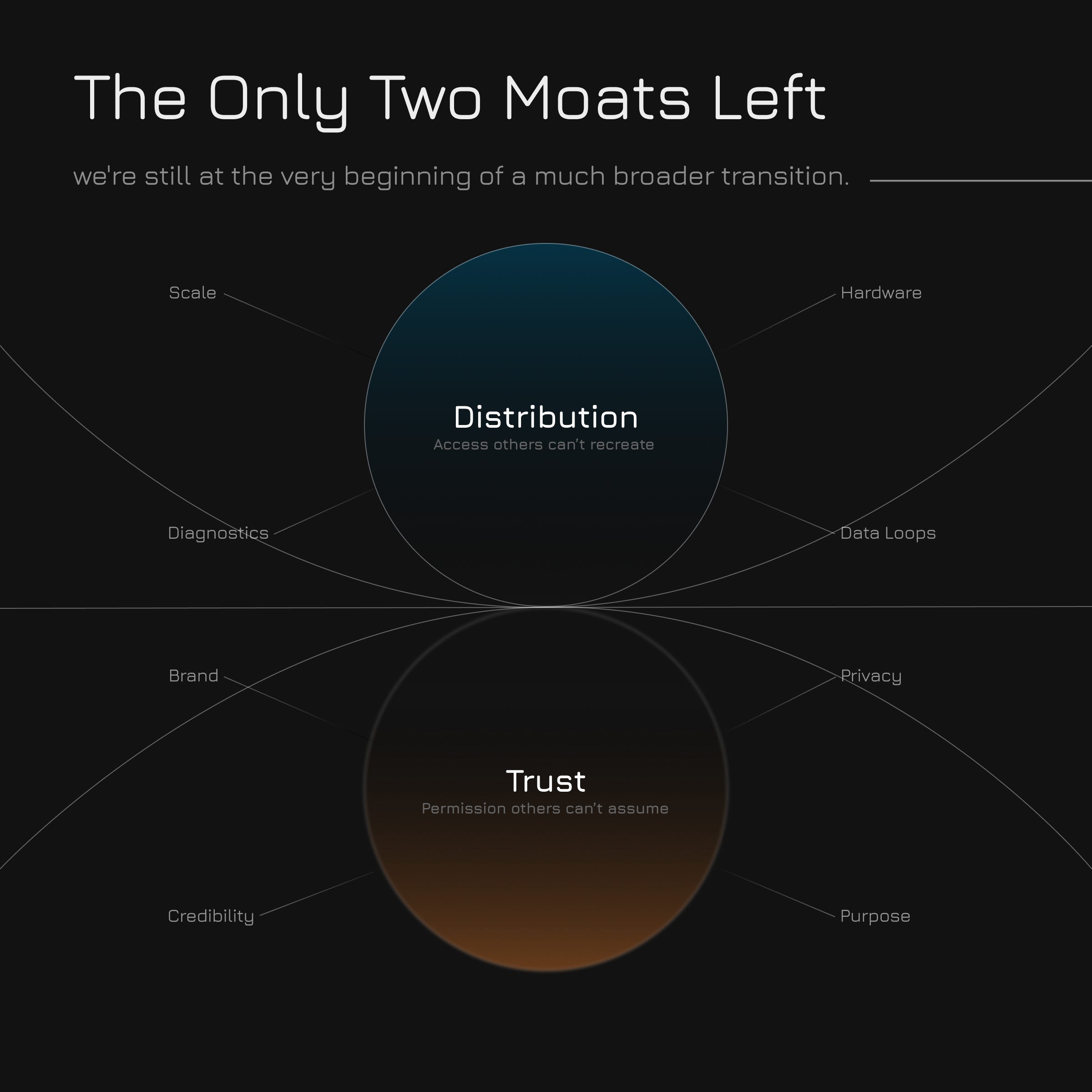

The Only Two Moats Left

I think there are only two durable moats left: distribution and trust.

What’s interesting is that distribution itself comes in two flavours.

The first is scale. If you acquire enough users quickly enough, distribution itself becomes the moat. That’s incredibly difficult to achieve, but we’ve seen plenty of companies where scale alone turns into a durable competitive advantage.

The second form is much more compelling, particularly in healthcare, because it builds directly on the idea that software alone is no longer enough. Distribution here is about having a unique way of collecting data or interacting with customers that nobody else has, which in turn creates a more differentiated and often much stickier advantage. There’s also nuance to it. It might be hardware that enables the generation of data that nobody else can access, or the ability to integrate into existing healthcare or insurance systems in a way that creates deep, hard-to-displace relationships.

A wearable is a good example of how this plays out in practice. The hardware isn’t simply the product, it’s also the distribution. It creates a continuous relationship with the user and generates proprietary health data that another company can’t simply recreate by building better software. The same logic applies to diagnostics companies, medical devices or businesses that own unique relationships with patients.

That said, I do think there’s a valid counterpoint here. Selling more and more general-purpose wearables likely becomes incrementally harder over time as the market saturates and devices like Whoop or Oura capture a large share of consumer attention. But I still think there’s a lot of value in more specialised wearables, particularly for specific populations, that measure things existing devices can’t. In those cases, the distribution isn’t just around scale, it’s owning a unique data stream that remains difficult to replicate.

That’s important because one of the arguments people make is that OpenAI or Anthropic could eventually build many of the same capabilities that today’s health companies are building. Technically, they probably could. But they don’t have the hardware. They don’t own the diagnostics infrastructure. They don’t have those proprietary ways of collecting data. That’s the key difference. Of course, if they wanted to own all those metrics, they have the capital and capabilities to do so, but for many of them, I don’t think they want to go deep into distribution at the focal layer. I think they want to be the intelligence that sits beneath all industries because that’s a much higher-leverage move.

The second moat is trust, and healthcare is probably the easiest place to see why that matters. A useful way to think about it is why someone would trust a clinic with years of blood work but hesitate to hand the same information to OpenAI. Part of that is probably data privacy, but if we’re realistic, I think it’s mostly brand and trust.

Take Function Health as an example. It exists to improve your health. That’s what people expect it to do. You don’t spend time wondering what else they’re trying to do with your data because the purpose of the business is clear. This becomes even more critical in preventive health, where much of the market sits outside traditional regulation and the trust gap is significantly wider. When there isn’t a strong regulatory framework guiding behaviour, consumers rely much more heavily on brand and perceived intent.

Deloitte’s latest research shows trust remains one of the strongest factors influencing whether consumers are willing to adopt generative AI in healthcare, which reinforces the idea that trust isn’t simply good branding. As software becomes easier for everyone to build, trust increasingly becomes part of the product itself, and that trust is built through a consistent, end-to-end experience across every touchpoint a user has with the company.

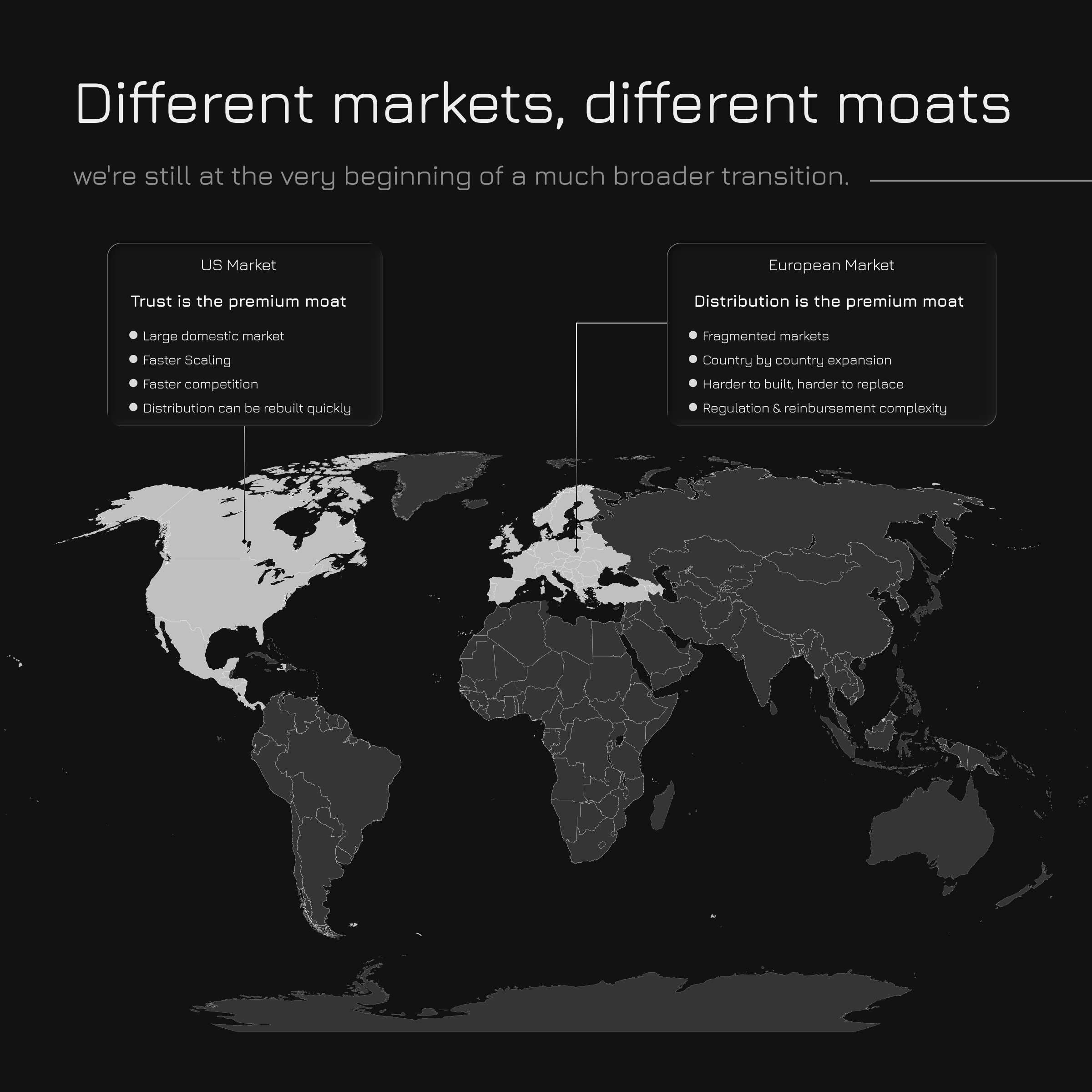

Different Markets, Different Moats

The key point is that those two moats don’t have the same value everywhere. People often ask me about the strengths and weaknesses of building healthcare companies in Europe versus the US, but I actually think they’re optimising for different things.

The US is incredibly good at speed. Consumers are generally more willing to pay directly for healthcare, venture capital moves faster and, if a business model works, companies can scale remarkably quickly across one large domestic market. The US spends close to 18% of GDP on healthcare, more than any other developed economy, creating an enormous commercial market for new healthcare products. That creates incredible opportunities, but it also means competition moves incredibly quickly.

Ironically, I think that’s exactly why distribution becomes less valuable in the US. Because it’s easier to build, it’s also easier to displace. You can already see this happening across preventive health. Prenuvo spent years largely defining the whole-body MRI category before competitors such as Ezra entered the market with lower-cost and potentially lower-resolution offerings that aggressively target the majority of use cases.

That’s what happens when markets commercialise quickly. Categories emerge faster, but they also become competitive faster. A competitor can build similar software. A business can often raise enough capital to acquire customers. Building years of credibility around a trusted health brand is much harder. That’s why I increasingly think trust becomes the more valuable moat in the US.

Europe feels almost like the opposite. Healthcare isn’t one market. It’s dozens of different markets. Regulation changes from country to country, reimbursement changes, languages change and healthcare systems themselves are structured differently. Consumers are also generally less willing to pay directly for healthcare, which means companies are often more dependent on insurers or employers to access the market.

Building a healthcare company often means expanding country by country and insurer by insurer rather than simply scaling across one unified market. The OECD has repeatedly identified fragmented regulation, governance and health data infrastructure as some of the biggest barriers preventing digital health companies from scaling across Europe.

Most founders experience that as friction. But I think investors should see exactly the same thing as defensibility. If distribution takes years to build, it also becomes much harder to replace. Part of that is simply the nature of the relationships you’re building. If you achieve the same level of distribution in Europe, the number of decision makers is much narrower and those relationships are much easier to maintain over time. Insurers, for example, are far less likely to switch providers quickly than individual consumers.

If you’ve spent years establishing those relationships, navigating multiple healthcare systems and expanding market by market, you’ve created something that another company can’t simply replicate with better software. What feels like Europe’s biggest weakness while you’re building often becomes one of its biggest strengths once you’ve built it.

That’s why I think the value of the moat changes depending on geography. In the US, I’d increasingly over index trust because distribution can be displaced much more quickly. In Europe, I’d increasingly over index distribution because it’s extraordinarily difficult to build and, once you’ve built it, it’s extraordinarily difficult to replace.

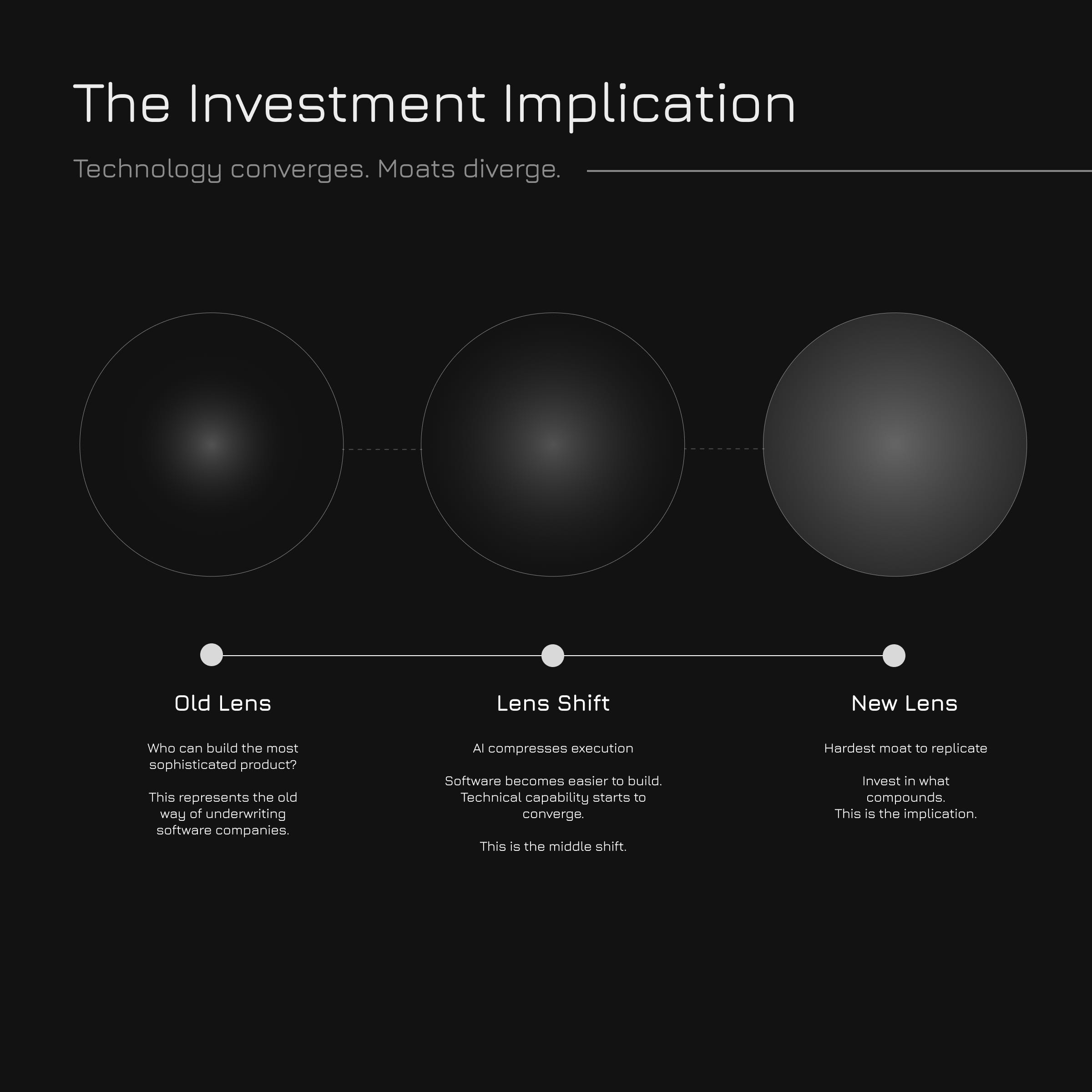

The Investment Implication

If our assumption is right that AI continues reducing the value captured by software, I think investors need to start looking at healthcare companies differently.

The question becomes much less about who can execute best or build the most sophisticated software, and much more about who can build trust and create differentiated distribution. A huge part of that is understanding where markets are going and positioning ahead of that shift, rather than simply being able to execute once the direction is already clear.

On another side as well, trust is something that can really only be built over years, which makes it a true compounding asset. The flip side, though, is that it’s also fragile. If you misstep, you can destroy it very quickly, unlike distribution. That tension is exactly what makes it so valuable in markets where everything else can be replicated quickly.

If you take that logic through to its conclusion, I think there are only two answers: distribution and trust. In Europe, I’d pay for distribution because it’s much harder to build and therefore much harder to displace. In the US, I’d pay for trust because software can be copied, capital can be raised and distribution can be rebuilt remarkably quickly.

The underlying technology will increasingly become similar. The moats won’t.

I’m now working on my third health tech company. I remember, even 10-15 years ago, investors saying that there was no competitive advantage to software. in fact, I remember being somewhat frustrated that they spent so little time paying any attention to the product we’d put so much work into.

The language was a bit different - everyone talked about traction and stickiness rather than trust and distribution. But the take away was the same.

Yes, you’ve got to build that good product to attract lots of people people (scale, distribution, traction) and then show value and create stickiness (trust, retention, high switching costs).

It seems the issues are still largely the same. Yes, AI brings the costs down of buidling software. But it’s got to actually be good. And a lot of it isn’t. That’s not a fault of AI. That’s a fault of whomever is directing the AI.

Do you think it’s possible that this is just another flavor of what’s always been true?